Oil prices rose on Thursday as U.S. implied consumer petroleum demand surged to a record high in the world’s top oil consumer even as the omicron variant of coronavirus threatens to dent oil consumption globally.

A signal by the U.S. Federal Reserve to tackle inflation before it derails the U.S. economy also boosted prices.

Brent crude oil futures rose by 80 cents, or 1.1%, to $74.68 a barrel by 0116 GMT, while U.S. West Texas Intermediate (WTI) crude futures increased by 88 cents, or 1.2%, to $71.75.

“Despite the current virus surge, the weekly EIA oil inventory report showed demand for petroleum products hit a record high, crude exports bounced back and national crude stocks posted a larger-than-expected draw,” said Edward Moya, senior analyst at OANDA.

“This current Omicron wave may lead to limited restrictive measures across the U.S., but lockdowns that happened during the peak of the pandemic will not be revisited.”

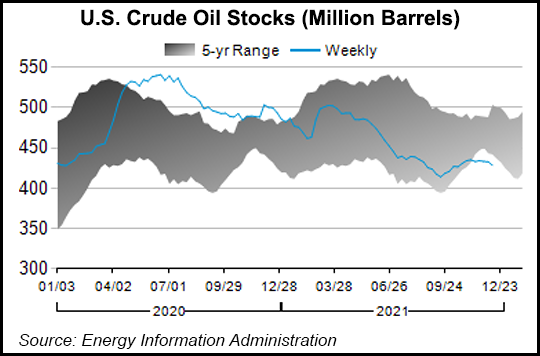

U.S. crude inventories sank by 4.6 million barrels in the week to Dec. 10, data from the U.S. Energy Information Administration showed. That was more than double expectations in a Reuters poll for a 2.1 million-barrel drop.

Product supplied by refineries, a proxy for demand, surged in the most recent week to 23.2 million barrels per day (bpd), due to gains in gasoline, diesel and other refined products.

Analysts said the rise reflects both expectations for a surge of people travelling for the holidays and the loosening of supply-chain bottlenecks that has more trucks on the road delivering goods.

Meanwhile, the Federal Reserve said it would end its pandemic-era bond purchases in March and begin raising interest rates as unemployment remains low and inflation has climbed.

Lingering worries about coronavirus curbed price gains.

Britain and South Africa reported record daily Covid-19 cases with omicron spreading rapidly while many firms across the globe are now asking employees to work from home, which could also limit oil demand.

{kind=link}